One of the most important decisions you make when joining a super fund are the investment options in which your super is invested.

Super funds provide a menu of different investment options in which you can invest your money to grow your balance over time. The investment options choices you make over the course of your working life will play a substantial role in determining how much super you have when you retire.

People who join a super fund and do not choose an investment option(s) are allocated to a “default” investment option. Members can change their investment option(s) at any time.

Most super funds offer a range of investment options designed to cater for their members’ investment return and risk objectives. More conservative investment options (with higher allocations to cash and fixed interest) will involve less risk and returns are lower. Conversely, more aggressive investment options (with higher allocations to shares and property) involve higher risk and are more volatile in the short-term but over the longer-term yield higher investment returns.

Different investment options will be suitable at different career and life stages

Your decision to choose investment option(s) is not a ‘set and forget’ decision. Your objectives and needs will change through your working life and your life into retirement. For this reason, you should periodically review your investment choices.

There can be strong financial reasons for taking different approaches to your investment options depending on what stage your career is at, and in response to changes in personal circumstances.

Early in your career, retirement is further into the future meaning that you have time to consider more aggressive investment options.

As the independent Australian Securities and Investments Commission (ASIC) MoneySmart website says: “A higher growth option will have higher risk and experience more volatile returns over the short term, but will usually achieve higher returns over the long term. If you are at least 10 years from retirement, you might consider choosing a higher growth option as you have time to ride out the ups and downs in the market.”

Then, as you near retirement, ASIC MoneySmart suggests “you might decide to reduce your level of risk, as preserving your capital will become more important.”

Changes in personal circumstances – including marriage, divorce, children, the death of a spouse, personal health issues, the success or failure of a businesses and other investments you own or are involved in – may mean that the investment options you currently have in place and which were perfectly suited to your long term financial planning for retirement are no longer the best fit for your needs and the needs of your dependents, which is why it is important to regularly review the suitability of your super investment options.

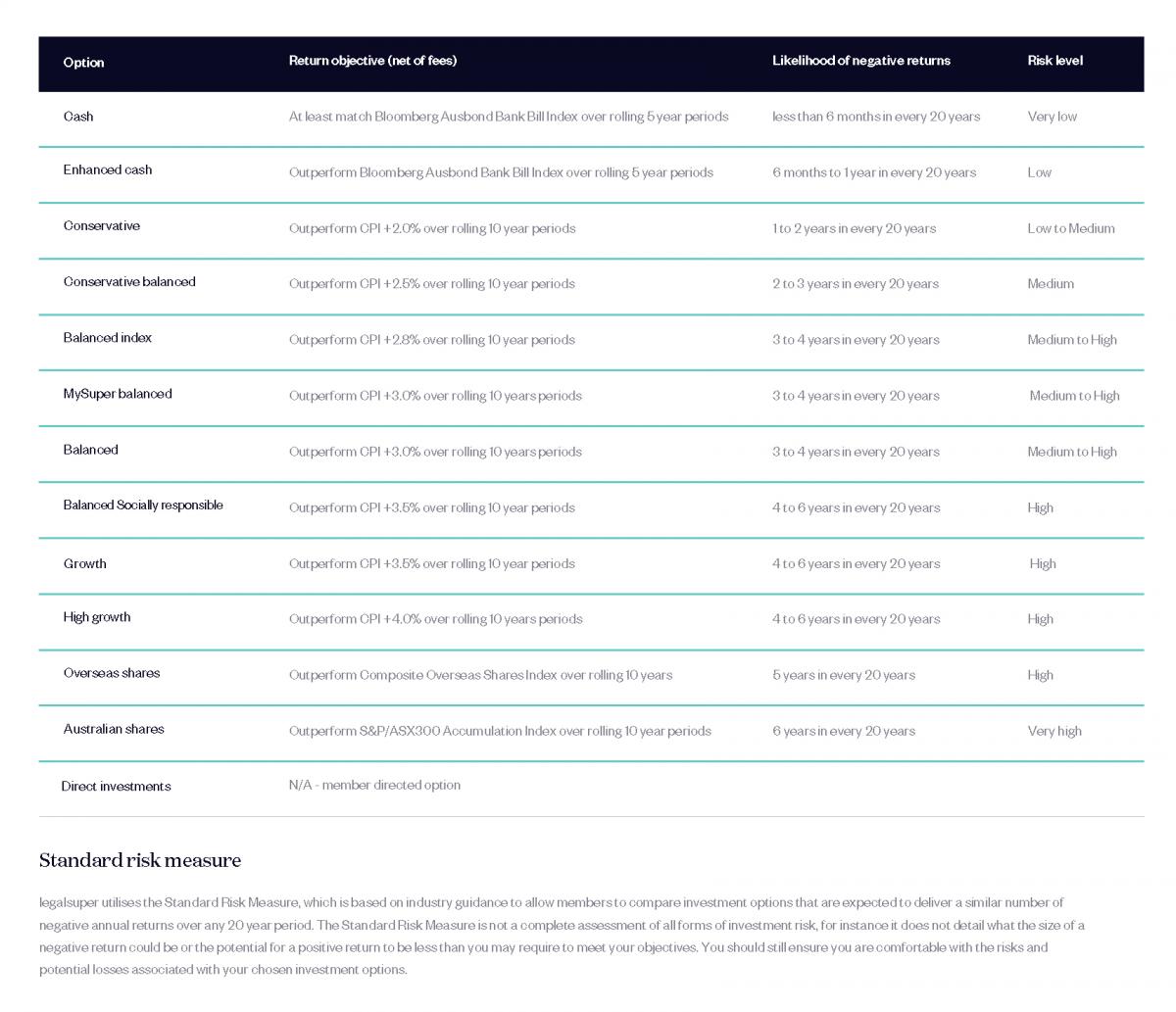

An example: legalsuper’s investment options:

Getting advice about investment options

Making decisions about your investment options which best meets your current and future needs can be challenging, but the difference between choosing a more suitable option as compared to a less suitable option can result in significantly different financial outcomes over the course of your working life.

The ASIC MoneySmart website offers members of the public a free Superannuation Calculator where they can estimate the different retirement benefit they may accrue based on the investment option they have chosen.

As the table below shows, based on the below assumptions, the Super Calculator show that the difference between the best and worst position is 39 per cent more in retirement savings.

| Calculator investment option | Balance at age 67 |

| Cash | $204,946 |

| Conservative | $232,702 |

| Moderate | $252,372 |

| Balanced | $266,556 |

| Growth | $271,951 |

| High growth | $283,931 |

Assumptions:

Starting age: 40, Income: $80,000, Retirement age: 67, Super balance: $45,000, Contributions: 9.5% employer, Fund fees level: Medium, All other standard assumptions unchanged.

However, making investment choices should never be solely about chasing a higher return. People need to feel comfortable with the choices they have made and the best way to accomplish this is to choose options which are compatible with your return objectives and risk tolerance.

When making these decisions, in the first instance you should call your super fund and discuss the types of super investment options on offer, your longer-term financial goals for retirement and your investment risk profile. Ideally, you would have this sort of conversation with your super fund every few years to ensure your choices remain aligned with your goals.

As ASIC MoneySmart notes: “Picking the right investment option within super is important whether you’re 16 or 65. Your investment strategy will influence how much money you’ll have to retire on and how you live your life in your retirement years.”

Finally, for many people super will be one of a number of components of their overall financial plan and it may also be advisable to consult your financial planner.

This information is of a general nature only and does not take into account your objectives, financial situation or needs. You should therefore consider the appropriateness of the information and obtain and read the relevant legalsuper Product Disclosure Statement before making any decision.

Legal Super Pty Ltd ABN 37 004 455 789, AFSL 246315 is the Trustee of legalsuper ABN 60 346 078 879.